Volatility: Defined in CryptoCurrency

Volatility is the measurement of how much the price of an asset is likely to change over a period of time. Stocks for established companies like Apple and Google have a much lower volatility than cryptocurrencies which may change a lot in one day.

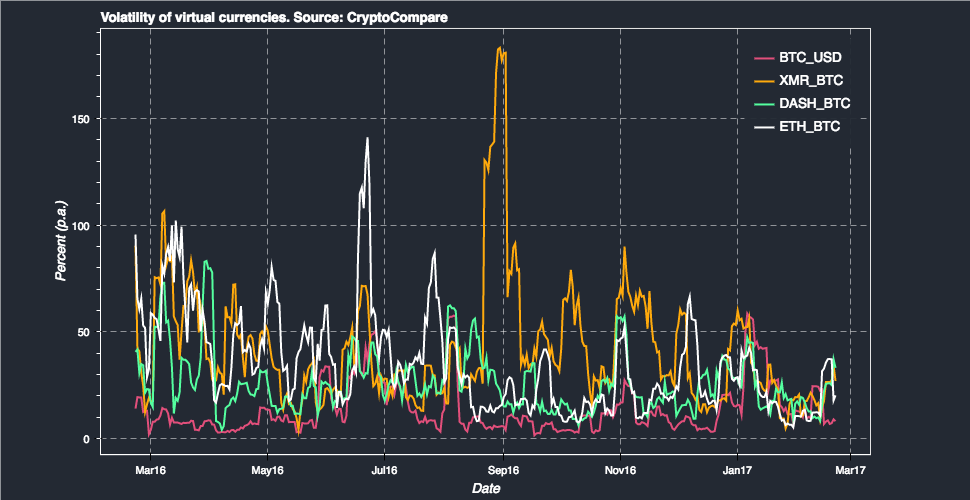

Volatility is a translation of what has cemented cryptocurrencies into internet indexing, since they exploded into the mainstream investor market has been their volatility.

The cryptocurrency market has also felt the ill effects of Bitcoin’s volatility because as a result of the price drops, Bitcoin’s trading volume, and even interest in the digital currency realm also decreases.

The danger is that volatility can cause a large exodus of investors to occur which severely dents the hopes of other cryptocurrencies gaining mass adoption status.

Volatility should be at the center of attention if there is to be a future in which crypto is used widely in day-to-day instances.

Volatility (finance)

The VIX In finance, volatility (symbol σ) is the degree of variation of a trading price series over time as measured by the standard deviation of logarithmic returns.

Historic volatility measures a time series of past market prices. Implied volatility looks forward in time, being derived from the market price of a market-traded derivative (in particular, an option).

Contents:123123

Volatility terminology

Volatility as described here refers to the actual volatility, more specifically:- actual current volatility of a financial instrument for a specified period (for example 30 days or 90 days), based on historical prices over the specified period with the last observation the most recent price.

- actual historical volatility which refers to the volatility of a financial instrument over a specified period but with the last observation on a date in the past

- near synonymous is realized volatility, the square root of the realized variance, in turn calculated using the sum of squared returns divided by the number of observations.

- actual future volatility which refers to the volatility of a financial instrument over a specified period starting at the current time and ending at a future date (normally the expiry date of an option).

- historical implied volatility which refers to the implied volatility observed from historical prices of the financial instrument (normally options)

- current implied volatility which refers to the implied volatility observed from current prices of the financial instrument

- future implied volatility which refers to the implied

volatility observed from future prices of the financial instrument

For a financial instrument whose price follows a Gaussian random walk, or Wiener process, the width of the distribution increases as time increases. This is because there is an increasing probability that the instrument's price will be farther away from the initial price as time increases. However, rather than increase linearly, the volatility increases with the square-root of time as time increases, because some fluctuations are expected to cancel each other out, so the most likely deviation after twice the time will not be twice the distance from zero.

Since observed price changes do not follow Gaussian distributions, others such as the Lévy distribution are often used.[1] These can capture attributes such as "fat tails". Volatility is a statistical measure of dispersion around the average of any random variable such as market parameters etc.

Mathematical definition

For any fund that evolves randomly with time, the square of volatility is the variance of the sum of infinitely many instantaneous rates of return, each taken over the nonoverlapping, infinitesimal periods that make up a single unit of time.Thus, "annualized" volatility σannually is the standard deviation of an instrument's yearly logarithmic returns.[2]

The generalized volatility σT for time horizon T in years is expressed as:

Volatility origin

Much research has been devoted to modeling and forecasting the volatility of financial returns, and yet few theoretical models explain how volatility comes to exist in the first place.Roll (1984) shows that volatility is affected by market microstructure.[3] Glosten and Milgrom (1985) shows that at least one source of volatility can be explained by the liquidity provision process. When market makers infer the possibility of adverse selection, they adjust their trading ranges, which in turn increases the band of price oscillation.[4]

Volatility for investors

Investors care about volatility for at least eight reasons:- The wider the swings in an investment's price, the harder emotionally it is to not worry;

- Price volatility of a trading instrument can define position sizing in a portfolio;

- When certain cash flows from selling a security are needed at a specific future date, higher volatility means a greater chance of a shortfall;

- Higher volatility of returns while saving for retirement results in a wider distribution of possible final portfolio values;

- Higher volatility of return when retired gives withdrawals a larger permanent impact on the portfolio's value;

- Price volatility presents opportunities to buy assets cheaply and sell when overpriced;

- Portfolio volatility has a negative impact on the compound annual growth rate (CAGR) of that portfolio

- Volatility affects pricing of options,

being a parameter of the Black–Scholes

model.

Volatility versus direction

Volatility does not measure the direction of price changes, merely their dispersion. This is because when calculating standard deviation (or variance), all differences are squared, so that negative and positive differences are combined into one quantity. Two instruments with different volatilities may have the same expected return, but the instrument with higher volatility will have larger swings in values over a given period of time.For example, a lower volatility stock may have an expected (average) return of 7%, with annual volatility of 5%. This would indicate returns from approximately negative 3% to positive 17% most of the time (19 times out of 20, or 95% via a two standard deviation rule). A higher volatility stock, with the same expected return of 7% but with annual volatility of 20%, would indicate returns from approximately negative 33% to positive 47% most of the time (19 times out of 20, or 95%). These estimates assume a normal distribution; in reality stocks are found to be leptokurtotic.

Volatility over time

Although the Black Scholes equation assumes predictable constant volatility, this is not observed in real markets, and amongst the models are Emanuel Derman and Iraj Kani's[5] and Bruno Dupire's local volatility, Poisson process where volatility jumps to new levels with a predictable frequency, and the increasingly popular Heston model of stochastic volatility.[6]It is common knowledge that types of assets experience periods of high and low volatility. That is, during some periods, prices go up and down quickly, while during other times they barely move at all.[7]

Periods when prices fall quickly (a crash) are often followed by prices going down even more, or going up by an unusual amount. Also, a time when prices rise quickly (a possible bubble) may often be followed by prices going up even more, or going down by an unusual amount.

Most typically, extreme movements do not appear 'out of nowhere'; they are presaged by larger movements than usual. This is termed autoregressive conditional heteroskedasticity. Whether such large movements have the same direction, or the opposite, is more difficult to say. And an increase in volatility does not always presage a further increase—the volatility may simply go back down again.

The risk parity weighted volatility of the three assets Gold, Treasury bonds and Nasdaq (Worldvolatility.com) acting as proxy for the Marketportfolio seems to have a low point at 4% after turning upwards for the 8th time since 1974 at this reading in the summer of 2014.worldvolatility.com

Alternative measures of volatility

Some authors point out that realized volatility and implied volatility are backward and forward looking measures, and do not reflect current volatility. To address that issue an alternative, ensemble measure of volatility was suggested.[8] This measure is defined as the standard deviation of ensemble returns instead instead of time series of returns.Implied volatility parametrisation

There exist several known parametrisation of the implied volatility surface, Schonbucher, SVI and gSVI.[9]Crude volatility estimation

Using a simplification of the above formula it is possible to estimate annualized volatility based solely on approximate observations. Suppose you notice that a market price index, which has a current value near 10,000, has moved about 100 points a day, on average, for many days. This would constitute a 1% daily movement, up or down.To annualize this, you can use the "rule of 16", that is, multiply by 16 to get 16% as the annual volatility. The rationale for this is that 16 is the square root of 256, which is approximately the number of trading days in a year (252). This also uses the fact that the standard deviation of the sum of n independent variables (with equal standard deviations) is √n times the standard deviation of the individual variables.

The average magnitude of the observations is merely an approximation of the standard deviation of the market index. Assuming that the market index daily changes are normally distributed with mean zero and standard deviation σ, the expected value of the magnitude of the observations is √(2/π)σ = 0.798σ. The net effect is that this crude approach underestimates the true volatility by about 20%.

Estimate of compound annual growth rate (CAGR)

Consider the Taylor series:Criticisms of volatility forecasting models

Performance of VIX (left) compared to past volatility (right) as 30-day volatility predictors, for the period of Jan 1990-Sep 2009. Volatility is measured as the standard deviation of S&P500 one-day returns over a month's period. The blue lines indicate linear regressions, resulting in the correlation coefficients r shown. Note that VIX has virtually the same predictive power as past volatility, insofar as the shown correlation coefficients are nearly identical.

Despite the sophisticated composition of most volatility forecasting models, critics claim that their predictive power is similar to that of plain-vanilla measures, such as simple past volatility [10][11] especially out-of-sample, where different data are used to estimate the models and to test them.[12] Other works have agreed, but claim critics failed to correctly implement the more complicated models.[13] Some practitioners and portfolio managers seem to completely ignore or dismiss volatility forecasting models. For example, Nassim Taleb famously titled one of his Journal of Portfolio Management papers "We Don't Quite Know What We are Talking About When We Talk About Volatility".[14] In a similar note, Emanuel Derman expressed his disillusion with the enormous supply of empirical models unsupported by theory.[15] He argues that, while "theories are attempts to uncover the hidden principles underpinning the world around us, as Albert Einstein did with his theory of relativity", we should remember that "models are metaphors – analogies that describe one thing relative to another".